Thuy’s Market Musings

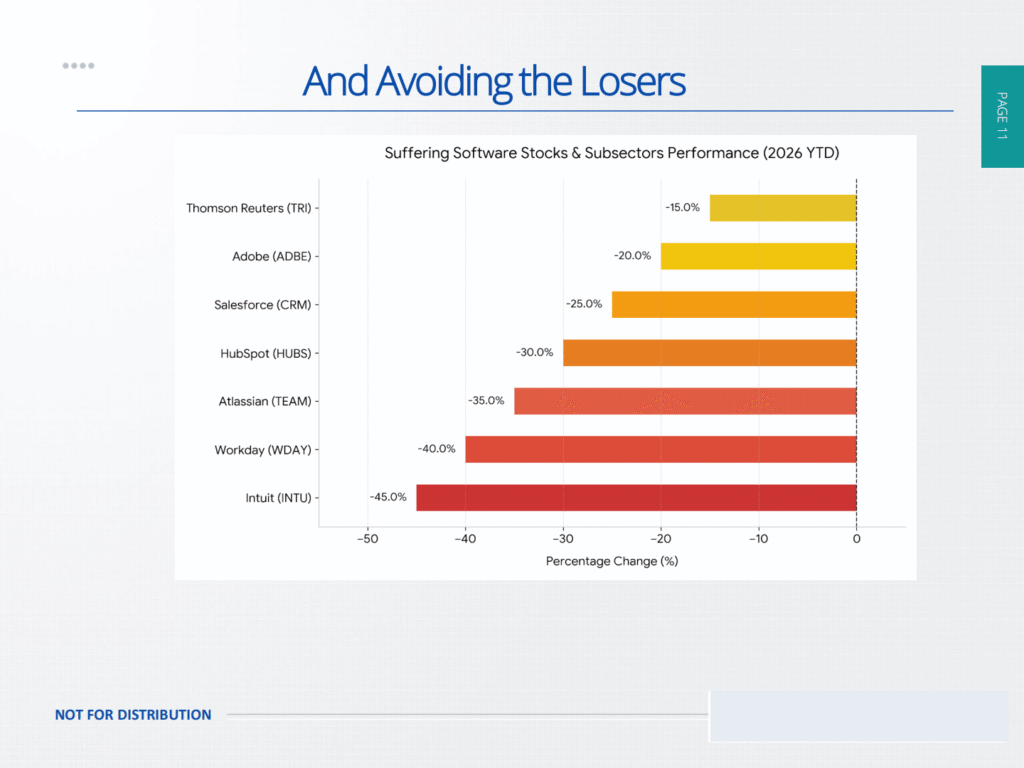

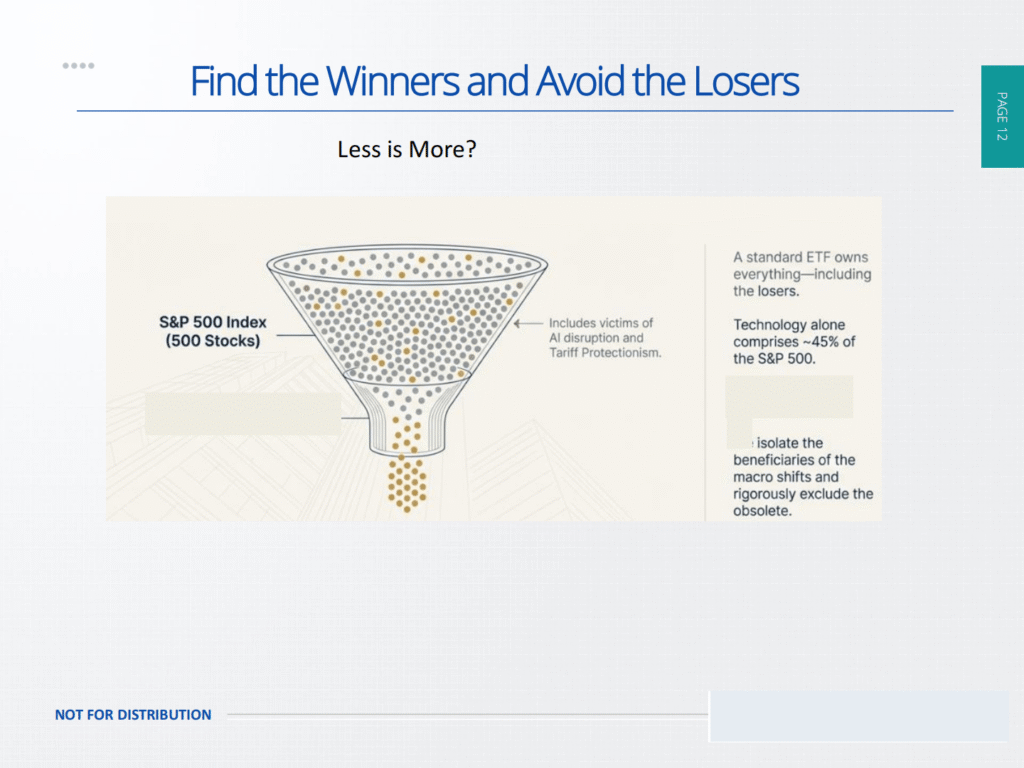

Investing in the AI ecosystem – Location Matters

Exploring how geography, talent, capital, infrastructure, and innovation hubs shape the future of AI-driven growth.

By Van Gordon, Thuy Tran – June 1, 2026

Event Overview

All information presented is informational and educational purposes only and is not intended for investment decisions. It does not constitute an offer to sell or a solicitation of an offer to buy any securities. Past Performance is not indicative of future results. Investing involves risk, including the potential loss of principal. The S&P 500 index is a market-capitalization weighted index of 500 of the largest publicly traded companies of the US.

Any views, strategies or products discussed in this material may not be appropriate for all individuals and are subject to risks. Investors may get back less than they invested, and past performance is not a reliable indicator of future results. Asset allocation/diversification does not guarantee a profit or protect against loss. Nothing in this material should be relied upon in isolation for the purpose of making an investment decision. You are urged to consider carefully whether the services, products, asset classes (e.g. equities, fixed income, alternative investments, commodities, etc.) or strategies discussed are suitable to your needs.

Meet the Speakers & Guests

Van Gordon

Agency Principle -Van Gordon Insurance and Financial Services

Thuy Tran

Chief Investment Officer at KUYR

Featured Moments

Relive the most memorable moments from the event.

Would you like to attend our next event?

Register to stay up to date and never miss important event information.

Invest Smart. Live Well.

Home » Storage for SoHoSoCal

Small Business Demands Legislation to Fight Growing Swipe Fees

The Hidden Tax on Main Street: Why Small Businesses Are Fighting Back Against Rising Swipe Fees

1. The Mechanics of the "Swipe Fee"

2. The Duopoly Problem: Visa and Mastercard

3. The Credit Card Competition Act (CCCA)

4. Why This Matters for the Consumer

- Raise Prices: Passing the fee onto the consumer.

- Surcharge: Adding a 3% fee at the register for credit card use.

- Minimums: Requiring a $10 or $15 minimum for card use, which can turn away customers.

5. The Soho SoCal Perspective: Protecting Your Bottom Line

- Evaluate Cash Discounts: Many states now allow “Dual Pricing” where you offer a lower price for cash/debit and a standard price for credit.

- Review Your Processor: Ensure you are on an “Interchange Plus” pricing model rather than “Tiered” pricing, which is often much more expensive for small businesses.

- Join the Advocacy: Follow the NFIB’s efforts on the CCCA. Your voice as a local business owner carries significant weight with Congressional representatives.

Popular Posts

Popular Posts

Home » Storage for SoHoSoCal

Celebrating the 12th Annual Orange County World Trade Week

1. Key Insights from the Global Frontier

- Technology in Logistics: Hearing from Luis Eraña (CEO of Alba Wheels Up) regarding the integration of AI in global logistics was eye-opening. It is clear that data-driven precision is becoming the backbone of successful supply chains.

- The State of Our Ports: An update on the Port of Los Angeles provided a clear picture of the infrastructure that keeps our local economy moving and connected to the world.

- Trade Policy & Advocacy: The discussions surrounding the USMCA and the update on Foreign Trade Zones are crucial for any business owner looking to scale and protect their operations in today’s volatile market.

2. The Power of Diplomacy and Relationships

3. Committing to Excellence

Popular Posts

Popular Posts

Home » Storage for SoHoSoCal

SBA Announces New $50 Million Grant Opportunity to Support Made in America Manufacturing, Workforce Training

“America’s reindustrialization is accelerating under the leadership of President Donald J. Trump, and the SBA is proud to stand with the small manufacturers driving that resurgence,” said SBA Administrator Kelly Loeffler. “As I travel the country and meet with these builders, innovators, and job creators, I’ve seen firsthand the essential role they play in restoring American industrial strength. Through this targeted initiative, we are equipping them with the resources and workforce support they need to grow, reshore critical supply chains, and help secure America’s position as a global manufacturing powerhouse for generations to come.”

- Be a for-profit or not-for-profit entity (including, but not limited to small businesses, other than small businesses, trade and professional associations, and educational institutions).

- Been in existence continually for at least the past three years.

- Have experience providing technical assistance, tools, or training, etc. relating to small manufacturing businesses on a regional or national basis.

- Demonstrate that it has the capacity to provide hands-on manufacturing-related training and technical assistance to small business concerns.

The Empower to Grow program, formerly known as 7(j) Management and Technical Assistance program, provides eligible U.S. small businesses with free business courses, tailored training, and one-on-one consulting to support their growth, operations, hiring, regulatory compliance, and government contracting competitiveness. The Empower to Grow program uplifts businesses to be procurement ready for federal, state, and local government contracts. For more questions about the Empower to Grow program, visit: Empower to Grow Program.

About the U.S. Small Business Administration

Popular Posts

Preparedness for Small Businesses

Outsmart Disaster is your preparedness partner. We guide you step by step through creating a Resiliency Roadmap so you can plan during the calm and bounce back when things get tough. We also provide business preparedness tips and recovery resources.

Together, we can be ready for

any interruptions.

Empowering Small Businesses to Prepare in Blue Skies, and Recover from Gray Skies

Every $1 Invested in Disaster Mitigation Saves $13 in Recovery1

40% of Businesses do not Reopen Immediately After Disasters2

An Additional 25% Close Within 12 Months3

Outsmart Disaster’s

RESILIENCY ROADMAP

Recognize Potential Threats: Identify, prioritize, and document risks unique to your business

Establish Clear Communication Channels: Gather contacts, plan communication, and set up emergency alerts

Understand Your Operations: Prioritize processes, document equipment, and secure IT systems.

Hazard Mitigation Planning: Assess building safety, inventory, backups, and safety features

Understand Your Insurance and Finances: Review insurance, plan finances, and explore disaster relief options

Create and Test Emergency Response Plan: Train employees, test plans, and prepare an emergency kit

Certified Trainer Interest Form

Do you work with small businesses and entrepreneurs? Become an Outsmart Disaster Certified Trainer. This program is designed for community-based organizations, chambers, local agencies, and trainers that support small businesses and want to deliver Outsmart Disaster resiliency training in their communities.

Disclaimer

Outsmart Disaster is a disaster awareness campaign that includes a no-cost business continuity training program offered by the California Office of the Small Business Advocate (CalOSBA). CalOSBA employees support the program in a training capacity only. CalOSBA does not make any recommendations or guarantees and assumes no responsibility concerning the activities of participating businesses. Participants, and not CalOSBA, are responsible for all plans created and any actions taken following the Outsmart Disaster training.

References

Popular Posts

Home » Storage for SoHoSoCal

Elevating Tradition: Mai Phat Mi Gia 2 Opens Its Doors in Little Saigon

If you’re in the heart of Little Saigon and seeking a Vietnamese dining experience that is both authentic and elevated, Mai Phat Mi Gia is a must-visit.

Here’s to a remarkable opening and a future filled with continued excellence.

Popular Posts

Home » Storage for SoHoSoCal

Why Health Care Costs Have Skyrocketed and What Congress Can Do

The Healthcare Crisis on Main Street: Why Costs Are Suraring and How Congress Can Fix It

Here is an in-depth look at the root causes of this crisis and the legislative roadmap for relief.

Part 1: Why Costs Have Skyrocketed

- The “Death Spiral” of the Small Group Market: The small group insurance market—where most small firms purchase coverage—is shrinking rapidly. Participation fell by 7.4% in just one year (2022–2023). As healthy groups leave the market for self-insurance or other options, the remaining “risk pool” becomes sicker and more expensive, causing premiums to spike by over 120% for some firms over the last two thập kỷ.

- Burdensome ACA Mandates: Federal regulations like the Essential Health Benefits requirement mandate that all small business plans cover ten specific categories, regardless of whether the employees need them. This “one-size-fits-all” approach eliminated more personalized, affordable plans that small businesses once used to manage costs.

- Lack of Transparency & Middlemen (PBMs): Pharmacy Benefit Managers (PBMs) act as middlemen between drug manufacturers and insurers. They often engage in “spread pricing”—charging the health plan a higher price for a drug than they pay the pharmacy and pocketing the difference. Because PBMs often profit more when drug prices are higher, they have little incentive to lower costs for small employers.

- Hospital Consolidation: Rapid consolidation in the healthcare industry has reduced competition. When large hospital systems buy up independent physician offices, they often add “facility fees” to the bill for the exact same services, driving up the cost of care for small business plans.

Part 2: What Congress Can Do (The 2026 Legislative Roadmap)

1. Increase Flexibility with CHOICE Arrangements

2. Pass the COMPETE Act (Short-Term Plans)

3. Level the Playing Field with "Site-Neutral" Payments

4. Ban Spread Pricing and Empower Transparency

5. Association Health Plans (AHPs)

Popular Posts

Home » Storage for SoHoSoCal

Small Business Cannot Afford Government-Run Health Care

1. The Staggering $500 Billion Price Tag

2. The Inefficiency of Government Management

- Longer Wait Times: Similar to other single-payer systems globally, elective and specialized procedures could see significant delays.

- Reduced Innovation: Private sector competition drives medical breakthroughs; a state monopoly could stifle the incentive for new treatments and technologies.

3. A Crushing Tax Burden on Employers

- Excise Taxes: Direct taxes on business activities.

- Payroll Taxes: Increasing the cost of every employee on the books, which could force small businesses to freeze hiring or reduce staff.

- Personal Income Tax Surcharges: A specific “State Personal Income CalCare Tax” that would target high-earners and business owners who file as individuals.