Home » Education Hub » Small Business Guidance

Small Business Demands Legislation to Fight Growing Swipe Fees

The Hidden Tax on Main Street: Why Small Businesses Are Fighting Back Against Rising Swipe Fees

1. The Mechanics of the "Swipe Fee"

2. The Duopoly Problem: Visa and Mastercard

3. The Credit Card Competition Act (CCCA)

4. Why This Matters for the Consumer

- Raise Prices: Passing the fee onto the consumer.

- Surcharge: Adding a 3% fee at the register for credit card use.

- Minimums: Requiring a $10 or $15 minimum for card use, which can turn away customers.

5. The Soho SoCal Perspective: Protecting Your Bottom Line

- Evaluate Cash Discounts: Many states now allow “Dual Pricing” where you offer a lower price for cash/debit and a standard price for credit.

- Review Your Processor: Ensure you are on an “Interchange Plus” pricing model rather than “Tiered” pricing, which is often much more expensive for small businesses.

- Join the Advocacy: Follow the NFIB’s efforts on the CCCA. Your voice as a local business owner carries significant weight with Congressional representatives.

Popular Posts

Home » Education Hub » Small Business Guidance

SBA Announces New $50 Million Grant Opportunity to Support Made in America Manufacturing, Workforce Training

“America’s reindustrialization is accelerating under the leadership of President Donald J. Trump, and the SBA is proud to stand with the small manufacturers driving that resurgence,” said SBA Administrator Kelly Loeffler. “As I travel the country and meet with these builders, innovators, and job creators, I’ve seen firsthand the essential role they play in restoring American industrial strength. Through this targeted initiative, we are equipping them with the resources and workforce support they need to grow, reshore critical supply chains, and help secure America’s position as a global manufacturing powerhouse for generations to come.”

- Be a for-profit or not-for-profit entity (including, but not limited to small businesses, other than small businesses, trade and professional associations, and educational institutions).

- Been in existence continually for at least the past three years.

- Have experience providing technical assistance, tools, or training, etc. relating to small manufacturing businesses on a regional or national basis.

- Demonstrate that it has the capacity to provide hands-on manufacturing-related training and technical assistance to small business concerns.

The Empower to Grow program, formerly known as 7(j) Management and Technical Assistance program, provides eligible U.S. small businesses with free business courses, tailored training, and one-on-one consulting to support their growth, operations, hiring, regulatory compliance, and government contracting competitiveness. The Empower to Grow program uplifts businesses to be procurement ready for federal, state, and local government contracts. For more questions about the Empower to Grow program, visit: Empower to Grow Program.

About the U.S. Small Business Administration

Popular Posts

Preparedness for Small Businesses

Outsmart Disaster is your preparedness partner. We guide you step by step through creating a Resiliency Roadmap so you can plan during the calm and bounce back when things get tough. We also provide business preparedness tips and recovery resources.

Together, we can be ready for

any interruptions.

Empowering Small Businesses to Prepare in Blue Skies, and Recover from Gray Skies

Every $1 Invested in Disaster Mitigation Saves $13 in Recovery1

40% of Businesses do not Reopen Immediately After Disasters2

An Additional 25% Close Within 12 Months3

Outsmart Disaster’s

RESILIENCY ROADMAP

Recognize Potential Threats: Identify, prioritize, and document risks unique to your business

Establish Clear Communication Channels: Gather contacts, plan communication, and set up emergency alerts

Understand Your Operations: Prioritize processes, document equipment, and secure IT systems.

Hazard Mitigation Planning: Assess building safety, inventory, backups, and safety features

Understand Your Insurance and Finances: Review insurance, plan finances, and explore disaster relief options

Create and Test Emergency Response Plan: Train employees, test plans, and prepare an emergency kit

Certified Trainer Interest Form

Do you work with small businesses and entrepreneurs? Become an Outsmart Disaster Certified Trainer. This program is designed for community-based organizations, chambers, local agencies, and trainers that support small businesses and want to deliver Outsmart Disaster resiliency training in their communities.

Disclaimer

Outsmart Disaster is a disaster awareness campaign that includes a no-cost business continuity training program offered by the California Office of the Small Business Advocate (CalOSBA). CalOSBA employees support the program in a training capacity only. CalOSBA does not make any recommendations or guarantees and assumes no responsibility concerning the activities of participating businesses. Participants, and not CalOSBA, are responsible for all plans created and any actions taken following the Outsmart Disaster training.

References

Popular Posts

Home » Education Hub » Small Business Guidance

Why Health Care Costs Have Skyrocketed and What Congress Can Do

The Healthcare Crisis on Main Street: Why Costs Are Suraring and How Congress Can Fix It

Here is an in-depth look at the root causes of this crisis and the legislative roadmap for relief.

Part 1: Why Costs Have Skyrocketed

- The “Death Spiral” of the Small Group Market: The small group insurance market—where most small firms purchase coverage—is shrinking rapidly. Participation fell by 7.4% in just one year (2022–2023). As healthy groups leave the market for self-insurance or other options, the remaining “risk pool” becomes sicker and more expensive, causing premiums to spike by over 120% for some firms over the last two thập kỷ.

- Burdensome ACA Mandates: Federal regulations like the Essential Health Benefits requirement mandate that all small business plans cover ten specific categories, regardless of whether the employees need them. This “one-size-fits-all” approach eliminated more personalized, affordable plans that small businesses once used to manage costs.

- Lack of Transparency & Middlemen (PBMs): Pharmacy Benefit Managers (PBMs) act as middlemen between drug manufacturers and insurers. They often engage in “spread pricing”—charging the health plan a higher price for a drug than they pay the pharmacy and pocketing the difference. Because PBMs often profit more when drug prices are higher, they have little incentive to lower costs for small employers.

- Hospital Consolidation: Rapid consolidation in the healthcare industry has reduced competition. When large hospital systems buy up independent physician offices, they often add “facility fees” to the bill for the exact same services, driving up the cost of care for small business plans.

Part 2: What Congress Can Do (The 2026 Legislative Roadmap)

1. Increase Flexibility with CHOICE Arrangements

2. Pass the COMPETE Act (Short-Term Plans)

3. Level the Playing Field with "Site-Neutral" Payments

4. Ban Spread Pricing and Empower Transparency

5. Association Health Plans (AHPs)

Popular Posts

Home » Education Hub » Small Business Guidance

Small Business Cannot Afford Government-Run Health Care

1. The Staggering $500 Billion Price Tag

2. The Inefficiency of Government Management

- Longer Wait Times: Similar to other single-payer systems globally, elective and specialized procedures could see significant delays.

- Reduced Innovation: Private sector competition drives medical breakthroughs; a state monopoly could stifle the incentive for new treatments and technologies.

3. A Crushing Tax Burden on Employers

- Excise Taxes: Direct taxes on business activities.

- Payroll Taxes: Increasing the cost of every employee on the books, which could force small businesses to freeze hiring or reduce staff.

- Personal Income Tax Surcharges: A specific “State Personal Income CalCare Tax” that would target high-earners and business owners who file as individuals.

4. Exacerbating an Already Astronomical Cost of Doing Business

Popular Posts

Home » Education Hub » Small Business Guidance

Joins Coalition Fighting Lawsuit Abuse

Shakedown attorneys find new gold mine on the internet

Popular Posts

For Business Owner: Understanding Worker Compensation Insurance in CA

Worker Compensation insurance is a crucial aspect of employee welfare and business operations in California. This document aims to provide a comprehensive overview of Worker Compensation insurance, including its purpose, benefits, requirements, and the claims process. Understanding these elements is essential for both employers and employees to ensure a safe and compliant workplace.

What is Worker Compensation Insurance?

Worker Compensation insurance is a type of insurance that provides financial and medical benefits to employees who are injured or become ill as a direct result of their job. In California, this insurance is mandated by law for most employers, ensuring that workers receive necessary care and compensation without needing to prove fault.

Purpose of Worker Compensation Insurance

- For employees, it ensures that they receive medical treatment and wage replacement if they are injured on the job.

- For employers, it limits their liability in case of workplace injuries, as employees generally cannot sue their employers for work-related injuries if they are covered by Worker Compensation.

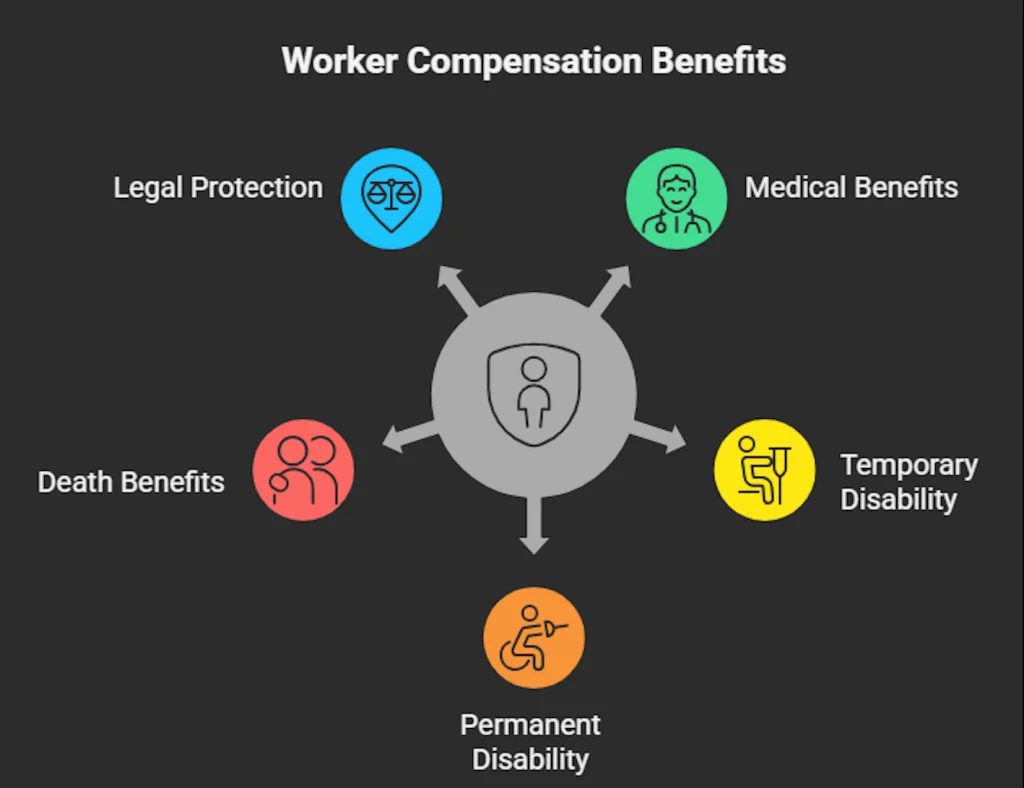

Benefits of Worker Compensation Insurance

- Medical Benefits: Covers medical expenses related to the injury or illness, including hospital visits, surgeries, and rehabilitation.

- Temporary Disability Benefits: Provides wage replacement for employees who are unable to work due to their injury or illness.

- Permanent Disability Benefits: Offers compensation for employees who suffer long-term or permanent impairments.

Death Benefits: Provides financial support to the dependents of employees who die as a result of a work-related injury or illness.

Legal Protection: Protects employers from lawsuits related to workplace injuries, as long as they have Worker Compensation insurance.

Requirements for Worker Compensation Insurance in California

- Mandatory Coverage: Employers with one or more employees must provide Worker Compensation insurance.

- Insurance Providers: Employers can purchase insurance from private insurance companies, or they can self-insure if they meet specific criteria set by the state.

- Posting Requirements: Employers must display a notice informing employees of their rights under Worker Compensation laws.

- Reporting Injuries: Employers are required to report any workplace injuries to their insurance provider promptly.

The Claims Process

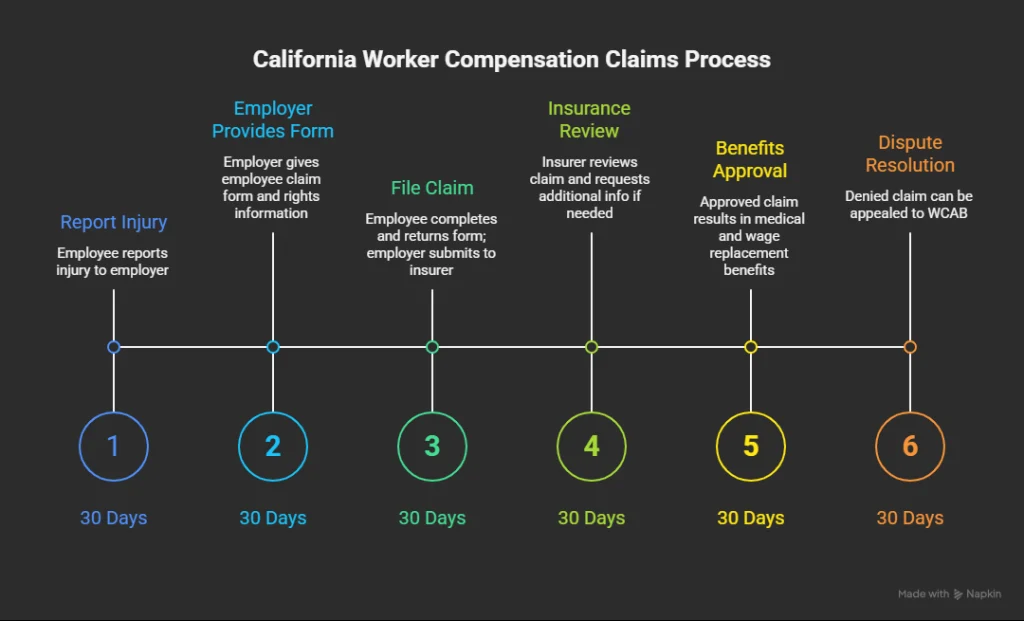

- Report the Injury: Employees must report their injury to their employer as soon as possible, ideally within 30 days.

- Employer’s Responsibilities: Once notified, the employer must provide the employee with a claim form (DWC 1) and information about their rights.

- Filing the Claim: The employee completes theclaim form and returns it to the employer, who then submits it to the insurance company.

Insurance Review: The insurance company reviews the claim and determines whether it is valid. They may request additional information or medical records.

- Benefits Approval: If the claim is approved, the employee will receive medical benefits and wage replacement as applicable.

- Dispute Resolution: If a claim is denied, the employee has the right to appeal the decision through the Workers’ Compensation Appeals Board (WCAB).

Common Misconceptions

- Only Physical Injuries are Covered: Many people believe that only physical injuries are covered under Worker Compensation. However, it also includes mental health issues and occupational diseases.

- You Can Sue Your Employer: While employees can sue third parties for negligence, they generally cannot sue their employer for work-related injuries if they are covered by Worker Compensation.

- Coverage is Optional: Some employers think that Worker Compensation insurance is optional, but it is mandatory for most businesses in California.

Conclusion

Popular Posts

Home » Education Hub » Small Business Guidance

The Best Time to Review Your Workers’ Comp Policy — Here’s Why

Did you know that January marks the highest volume of Workers’ Compensation policy renewals in the country?

This makes January a critical window when businesses actively review their coverage and look for better options. And this year, the timing is especially important. Here’s what’s happening in the market:

January = peak renewal season for Workers’ Compensation policies

Many other commercial insurance lines are seeing rate increases across multiple industries

Several competitors are increasing Workers’ Compensation rates, even for historically stable classes

However, there’s good news.

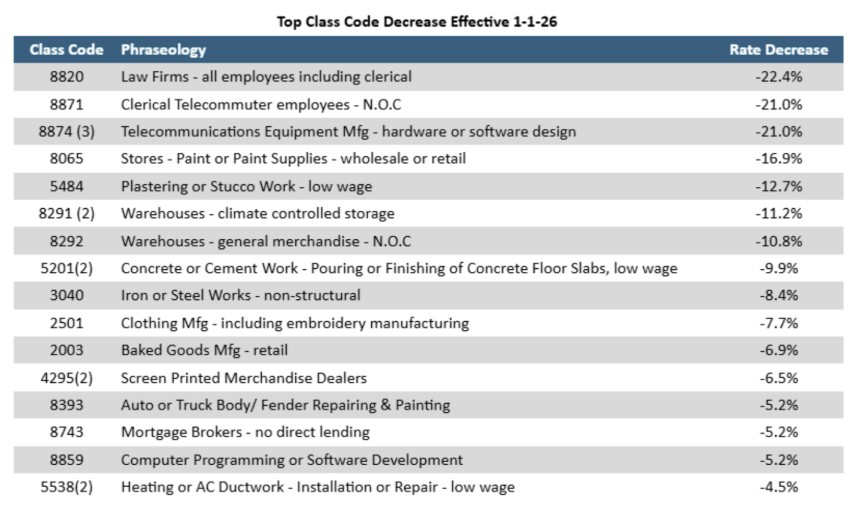

1. Rate Decreases for Select Industries - Effective January 1, 2026

While the overall California Workers’ Compensation rate is increasing by +1.5%, several key industries are seeing significant rate decreases effective:

- January 1, 2026 for new business

- January 1, 2026 for renewal business

We’ve attached a list of high-potential class codes and industries that are experiencing notable decreases, including professional services, manufacturing, warehousing, specialty trades, and more.

2. Why this matters to you

If your business falls under one of these class codes, you may be:

- Overpaying at renewal

- Missing an opportunity for immediate savings

- Renewing with a carrier that is increasing rates unnecessarily

A quick review of your Workers’ Compensation policy could result in meaningful premium savings—especially during this renewal window.

3. Next step

We encourage you to review your business classification and reach out to us to see if your industry qualifies for these lower rates. There is no obligation—just an opportunity to make sure your coverage and pricing are still working in your favor.

It is the best time to act. Let’s make sure you’re not leaving savings on the table.

Popular Posts

Home » Education Hub » Small Business Guidance

New funding opportunity from the State of California

We’re excited to share a new funding opportunity from the State of California that could support entrepreneurs and community-oriented small business initiatives across the state.

Social Entrepreneurs for Economic Development 3 (SEED 3)

This grant program aims to encourage and support entrepreneurship among individuals who face significant barriers to employment — particularly those with limited English proficiency and immigrants — by providing micro-grants, entrepreneurial training, and technical assistance to help start or sustain small businesses that address social needs in their communities. (California Grants Portal)

What the SEED 3 Grant Offers

- Purpose: Support entrepreneurs in launching or maintaining businesses that address community needs and social challenges. (California Grants Portal)

- Target populations: Individuals who face employment barriers, including those with limited English proficiency and non-citizens (including DACA or TPS recipients), as well as U.S. citizens within those groups. (California Grants Portal)

- Who can apply: Businesses, individuals, nonprofits, legal entities, public agencies, and tribal governments. (California Grants Portal)

- Total funding: Approximately $6,750,000 available statewide. (California Grants Portal)

Why this matters

- Encourages inclusive economic development

- Helps overcome barriers to business ownership and growth.

- Provides both financial support and valuable training.

Important Dates

- The grant is expected to open January 26, 2026. (California Grants Portal)

- Full application details and guidelines will be available at that time via the California Grants Portal.

This opportunity could be highly valuable for entrepreneurs ready to make a positive impact in their communities while building a sustainable business.

For full details, eligibility criteria, and application instructions, please visit the California Grants Portal. If you would like assistance reviewing your eligibility or preparing an application, feel free to reach out.

Popular Posts

Home » Education Hub » Small Business Guidance

New California Grant: Support for Small Businesses When Employees Take Paid Family Leave

As a small business owner in California, you know that when an employee takes time off to bond with a new child or care for a sick family member, the impact is felt across the entire team. While California’s Paid Family Leave (PFL) program helps your employees with wage replacement, the burden of covering their duties often falls on your shoulders—and your budget.

The good news? The Paid Family Leave Small Business (PFL SB 4) Grant is here to help you bridge that gap.

1. What is the PFL SB 4 Grant?

Administered by the California Employment Training Panel (ETP) and the Labor and Workforce Development Agency (LWDA), this grant program is designed to help small businesses offset the costs associated with an employee being out on PFL.

Whether you need to cross-train existing staff to pick up the slack or hire and train a temporary replacement, this grant provides direct financial relief to keep your operations running smoothly.

2. How Much Can You Receive?

The grant amount depends on the size of your workforce:

- Businesses with 1–50 employees: Eligible for $2,000 per employee utilizing PFL.

- Businesses with 51–100 employees: Eligible for $1,000 per employee utilizing PFL.

3. What Can the Funds Be Used For?

The grant is flexible, allowing you to cover various “out-of-pocket” costs that arise when an employee is on leave, including:

- Cross-training: Paying for the time and resources to train current employees to handle new duties.

- Upskilling: Improving the skills of remaining staff to ensure productivity doesn’t drop.

- Recruitment: Covering marketing and hiring costs if you need to bring in temporary help.

4. Is Your Business Eligible?

To qualify for the PFL SB 4 Grant, your business must meet the following criteria:

- Size: Employ between 1 and 100 employees.

- PFL Usage: Have at least one employee who is currently utilizing (or has recently utilized) the California PFL program.

- Registration: Be registered to do business in California and in “Active” status with the Secretary of State.

- Tax ID: Have an active California Employer Account Number (CEAN).

Note for PEO Users: If you use a Professional Employer Organization (PEO) for payroll, you are only eligible if your company is listed as the employer on the CEAN. If you file under the PEO’s account number, you may not qualify.

5. How to Apply

The application process is designed to be quick—typically taking about 15–20 minutes. You will need:

- Your 8-digit California Employer Account Number (CEAN).

- Your business’s NAICS code.

- The 10-digit EDD Customer Account Number of the employee on leave.

The current window for applications is open, but funds are often distributed on a first-come, first-served basis. If you have employees planning for leave or currently away, now is the time to act.

Apply or learn more at: